Krystal Biotech (KRYS)·Q4 2025 Earnings Summary

Krystal Biotech Crushes Q4 as VYJUVEK Hits $107M — EPS Beats by 52%

February 17, 2026 · by Fintool AI Agent

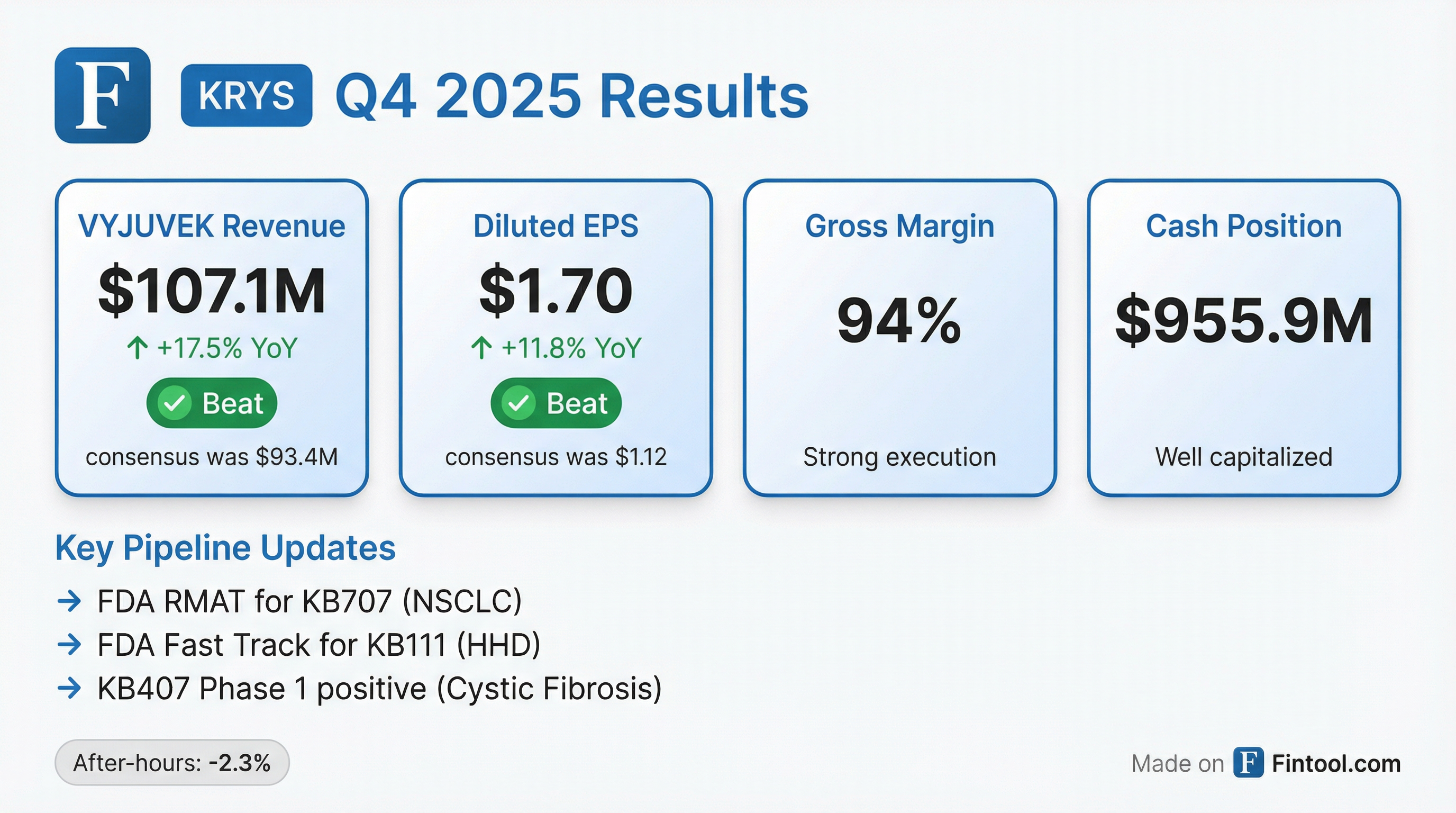

Krystal Biotech delivered a blowout Q4 2025, with VYJUVEK revenue of $107.1 million crushing consensus by 14.6% and diluted EPS of $1.70 beating estimates by over 50%. The gene therapy pioneer extended its consecutive beat streak to 8 quarters while securing key FDA designations for its pipeline programs. Shares traded down ~2% after-hours despite the strong results, suggesting investors may be taking profits after the stock's 125%+ run over the past year.

Did Krystal Biotech Beat Earnings?

Yes — decisively on both revenue and EPS.

This marks KRYS's eighth consecutive earnings beat — a testament to the commercial execution behind VYJUVEK, the first-ever redosable gene therapy approved in the U.S., Europe, and Japan.

What's Driving VYJUVEK Growth?

VYJUVEK's commercial success continues to accelerate:

- $107.1M in Q4 and $389.1M for FY 2025 — up 34% YoY

- $730M+ cumulative revenue since U.S. launch

- 660+ reimbursement approvals secured in the U.S. with strong nationwide access

- 500+ unique prescribers since launch with 50+ new prescribers added in Q4 2025

- Three consecutive quarters of reimbursement approval acceleration

- 90+ patients prescribed internationally across Germany, France, and Japan

The company continues international expansion with pricing negotiations progressing:

- Germany: Pricing agreement expected ~Q3 2026; revenue being accrued conservatively until finalized

- France: Operating under AP2 early access program; pricing not expected until 1H 2027

- Japan: Price negotiated (October 2025), but regulatory rules require two-week prescriptions in Year 1 — creating compliance burden that may normalize once Year 2 begins in late 2H 2026

- Italy: Launch targeted for 2H 2026 after pricing finalized — no accrual situation

- Distributor Network: 20+ country agreements, targeting 40+ countries by year-end 2026, now including Israel

VYJUVEK was awarded the Prix Galien in France in December 2025 for innovation and clinical impact — a significant validation during ongoing European reimbursement discussions.

Full Year 2025 Financial Summary

What Did Management Guide?

Management provided FY 2026 expense guidance but no specific revenue targets:

Note: Guidance excludes stock-based compensation, which the company said it cannot confidently estimate.

Key management commentary on 2026 outlook:

- Ex-US will be the predominant growth driver for 2026 revenue, though US demand continues to accelerate

- US utilization patterns evolving — some longer-tenured patients are transitioning to "start-stop" intermittent treatment cycles as their disease management stabilizes, making demand kinetics harder to predict

- Starting Q1 2026, the company will report US vs. ex-US revenue separately for the first time

- Revenue may not track linearly with patient counts this year due to accruals, timing effects, and ongoing pricing negotiations

Capital Allocation

On the earnings call, CEO Krish Krishnan addressed capital deployment priorities:

"We're not intending presently to use any of our cash towards in-licensing or buying any kind of third-party technology or company at the moment."

A potential stock buyback remains on the table, but the timeline depends on how larger indications (oncology, alpha-1, aesthetics) progress in terms of securing development or commercialization partners.

What's New in the Pipeline?

Krystal secured multiple regulatory wins and advanced clinical programs across four therapeutic areas:

Respiratory

KB407 (Cystic Fibrosis) — In January 2026, the company reported positive Phase 1 (CORAL-1) data confirming lung delivery and CFTR expression. Key findings from a diverse patient population including 4 modulator-ineligible patients:

- Transduction rates of 29-42% across all patients biopsied — exceeding targets

- All usable biopsies positive for transduction

- CFTR protein expression persisted for at least 96 hours — positive indicator for potential weekly dosing

- Encouraging apical CFTR expression observed in Class 1 patients

The company is working with the CFF TDN and FDA on repeat dosing study design and expects to initiate CORAL-3 registrational study in 1H 2026.

KB408 (Alpha-1 Antitrypsin Deficiency) — Actively enrolling patients in repeat dosing study. The study includes multiple bronchoscopies at baseline and after four weekly KB408 doses to assess additive effects on lung AAT and bound neutrophil elastase levels — key data points that will support accelerated approval discussions with FDA. Data update expected before year-end 2026.

Oncology

KB707 (NSCLC) — FDA granted RMAT (Regenerative Medicine Advanced Therapy) designation in February 2026 for advanced or metastatic non-small cell lung cancer. The company is enrolling patients in a dose expansion cohort of KYANITE-1 evaluating inhaled KB707 with chemotherapy, with interim efficacy data and registrational plans expected later this year.

Dermatology

KB111 (Hailey-Hailey Disease) — FDA granted Fast Track Designation in January 2026. The company expects to complete development of an HHD-specific evaluation scale in 1H 2026 and initiate a registrational study in 2H 2026.

Ophthalmology

KB803 (Corneal Abrasions in DEB) — Enrollment ongoing in Phase 3 IOLITE study with intensified three doses weekly regimen. Primary endpoint is change from baseline in average number of days per month with corneal abrasion symptoms in patients 6 months+ with genetically confirmed DEB. Enrollment completion expected 1H 2026 with top-line results before year-end.

KB801 (Neurotrophic Keratitis) — EMERALD-1 registrational study upsized to strengthen powering and increase the safety database in support of a potential streamlined filing. Dosing frequency intensified to daily administration to facilitate patient or caregiver administration in the home setting from launch. Data expected before year-end 2026.

How Did the Stock React?

Despite the strong beat, KRYS traded down ~2.3% after-hours to around $270 from a $276.45 close. This follows a remarkable run — the stock is up 125%+ over the past 12 months from ~$123 lows to recent highs near $296.

The muted reaction likely reflects:

- Profit-taking after the stock's significant appreciation

- Lack of explicit revenue guidance for FY 2026

- Extended timelines for international pricing negotiations (Germany through 2H 2026, France through 2027)

What Changed From Last Quarter?

The quarter saw continued commercial momentum with VYJUVEK while the pipeline achieved multiple regulatory milestones that could accelerate development timelines.

Balance Sheet Strength

Krystal ended Q4 2025 with a fortress balance sheet:

With nearly $1 billion in liquidity and a profitable commercial business, Krystal has ample runway to fund its pipeline through multiple registrational readouts without dilutive financing.

Q&A Highlights

On the 90 patient estimate outside the US:

"It's really difficult to estimate number of patients in Europe... the 90 number itself is somewhat of an approximation [based on bios shipped and pharmacies disclosed]... Starting in Q1, we'll have an idea of how U.S. is doing versus the rest of the world." — CEO Krish Krishnan

On ophthalmology dosing changes (KB801/KB803): Management explained that the shift to daily dosing for KB801 and 3x weekly for KB803 was deliberate to enable home administration while accounting for human error in self-dosing. The clean safety profile of both programs made this possible.

"Our concern is you want to make sure that if... there's a dose that doesn't get into the eye, they blink... So we thought it'd be easy. We have a very safe profile, and the drug is clean." — President of R&D Suma Krishnan

On KB801/KB803 enrollment: All 60 KB801 patients will be enrolled on the new once-daily regimen (none on the old weekly regimen). The company has 50% of its target 30 sites activated and expects the remainder within the next couple months.

Key Takeaways

-

VYJUVEK commercial momentum continues — $107M quarterly revenue with 94% gross margins demonstrates strong pricing power and durable demand in the dystrophic epidermolysis bullosa market

-

Pipeline validation expanding — Three FDA regulatory designations (RMAT for KB707, Fast Track for KB111, positive CF data with 96+ hour CFTR expression) reinforce the versatility of the HSV-1 gene delivery platform

-

2026 catalyst-rich — Multiple registrational readouts expected: KB803 (IOLITE), KB801 (EMERALD-1), KB407 (CORAL-3 initiation), KB707 (interim efficacy), KB111 (study initiation)

-

Financial strength — $956M cash position and profitability enable continued investment without shareholder dilution

-

International expansion progressing — While pricing timelines extend, the 40-country distributor network target and 90+ international patients signal global demand

See the full Q4 2025 8-K filing for complete financial statements and disclosures.

View KRYS company page for real-time data and document library.